By Aboubakr Kaira Barry, CFA, Managing Director, Results Associates, and Chair of the Omou Financial Literacy Center, Bethesda, Maryland, USA

Guinea’s balance of payments — the country’s annual scorecard of money coming in and going out, expressed in US dollars — tells a story that is more complex than the usual mining-boom narrative. It shows how much money comes into Guinea from all sources, not just mining, and how much leaves through imports, profit outflows, and other payments.

Foreign investors are clearly betting big on Guinea. Between 2020 and 2024, foreign direct investment — long-term money put into mines, infrastructure, and other productive assets — rose sharply, driven largely by bauxite, iron ore, and infrastructure linked to Simandou. That is an important sign of confidence, but it is only one part of the story.

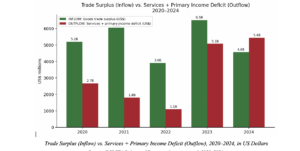

On the surface, Guinea’s export performance looks strong. Goods exports increased over the period, and the country maintained a large trade surplus, meaning it sold more goods abroad than it bought. Yet the current account — the broad measure of a country’s transactions with the rest of the world through trade, services, investment income, and transfers — weakened from surplus to deficit as outflows rose faster than inflows.

The reason is straightforward. Payments for imported services, especially technical and engineering services tied to major mining projects, increased sharply. At the same time, primary income — mainly profits sent abroad by foreign investors — also rose steeply. In effect, Guinea’s mines are generating more export revenue, but a large share of that money is leaving the country through service payments and profit repatriation.

.

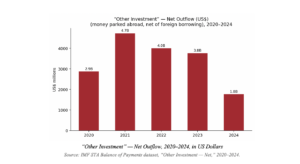

Another outflow comes from Guineans and companies based in Guinea. Under the “other investment” category in the balance of payments, they have been accumulating large assets abroad, mostly in the form of foreign bank deposits and other claims. This is not necessarily illegal, but without transparency, citizens cannot tell who is building these foreign assets or whether they reflect ordinary business decisions or something more problematic.

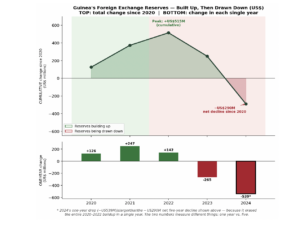

When these outflows are added to current account payments, Guinea’s total money outflow exceeded inflows in four of the last five years. This forced the central bank to use reserves as a buffer. Foreign exchange reserves — the central bank’s stock of foreign currency — initially rose, then fell sharply as they helped absorb this gap. Where extractive revenues are managed prudently, foreign exchange reserves usually strengthen over time rather than being repeatedly drawn down. A future reversal of the recent reserve losses would be one sign that Guinea’s mining boom is beginning to support long-term prosperity.

Guinea has nonetheless made real progress on extractive transparency. Guinea’s latest EITI Validation, in May 2026, gave it a “good” overall score of 73.5 points under the 2023 Standard, recognizing the country’s advances in publishing contracts and disclosing production and revenue data, including around Simandou. This gives Guinea a stronger transparency record than many resource-rich peers.

But an important gap remains: beneficial ownership transparency. Beneficial ownership means the real people who ultimately own or control a company and benefit from its profits, even when legal ownership sits behind layers of firms. Without a strong law and effective implementation, citizens and public institutions cannot clearly see who is behind the companies receiving mining-related revenues.

That matters because transparency is not only about contracts and production volumes. It is also about identifying who benefits from the wealth being generated, detecting conflicts of interest, and strengthening public trust. In a context where large sums are moving abroad, this visibility becomes even more important.

PEFA (Public Expenditure and Financial Accountability) is a standardized international diagnostic of how well governments manage public money, scored from A (best practice) to D (below basic, meaning minimum requirements are not met). Guinea’s most recent assessment, in 2019, rated the country D on financial data integrity and accounting — a serious weakness in the systems that should track mining revenues.

That is why the policy message is simple. First, Guinea should complete and implement a robust beneficial ownership framework covering all companies linked to extractive revenue flows. Second, it should strengthen its accounting, reporting, and oversight systems so that mining revenues can be fully traced from collection to final use.

Simandou and the wider mining boom will almost certainly deliver major infrastructure. But infrastructure alone does not guarantee broad prosperity. The real test is whether the revenues generated become visible, accountable, and well managed in ways that improve the lives of ordinary Guineans.